Swiss VAT calculation is based on three rates in effect since 1 January 2024: 8.1% (standard rate), 2.6% (reduced rate) and 3.8% (accommodation rate). To convert a net amount to gross, multiply it by 1.081 (standard rate). To find the net amount from a gross price, divide by 1.081. Use our Swiss VAT calculator below for instant results. For a comprehensive overview of VAT regulations and rates, see our guide to VAT in Switzerland in 2024 and 2025. My Swiss Company SA, Corporate Services Provider in Geneva, Lucerne and Zug, supports businesses with VAT calculation, filing and compliance in Switzerland.

Table of contents

- Online Swiss VAT calculator

- The 3 Swiss VAT rates in 2026

- Calculation formulas: net to gross and gross to net

- Effective method vs net tax rate method

- VAT registration: who is liable?

- VAT filing: schedule and obligations

- Planned VAT increase: funding the 13th OASI pension

- FAQ: Swiss VAT calculation

- Sources

Online Swiss VAT calculator

Select the type of goods or service, enter your amount and instantly obtain the applicable Swiss VAT calculation. The calculator includes all three official rates and allows you to simulate the projected rates linked to the funding of the 13th OASI pension.

Swiss VAT Calculator 2026

Rates in effect since 1 January 2024

Source: Federal Tax Administration (FTA) · Updated: April 2026

Need help with your VAT filings or registration in Switzerland?

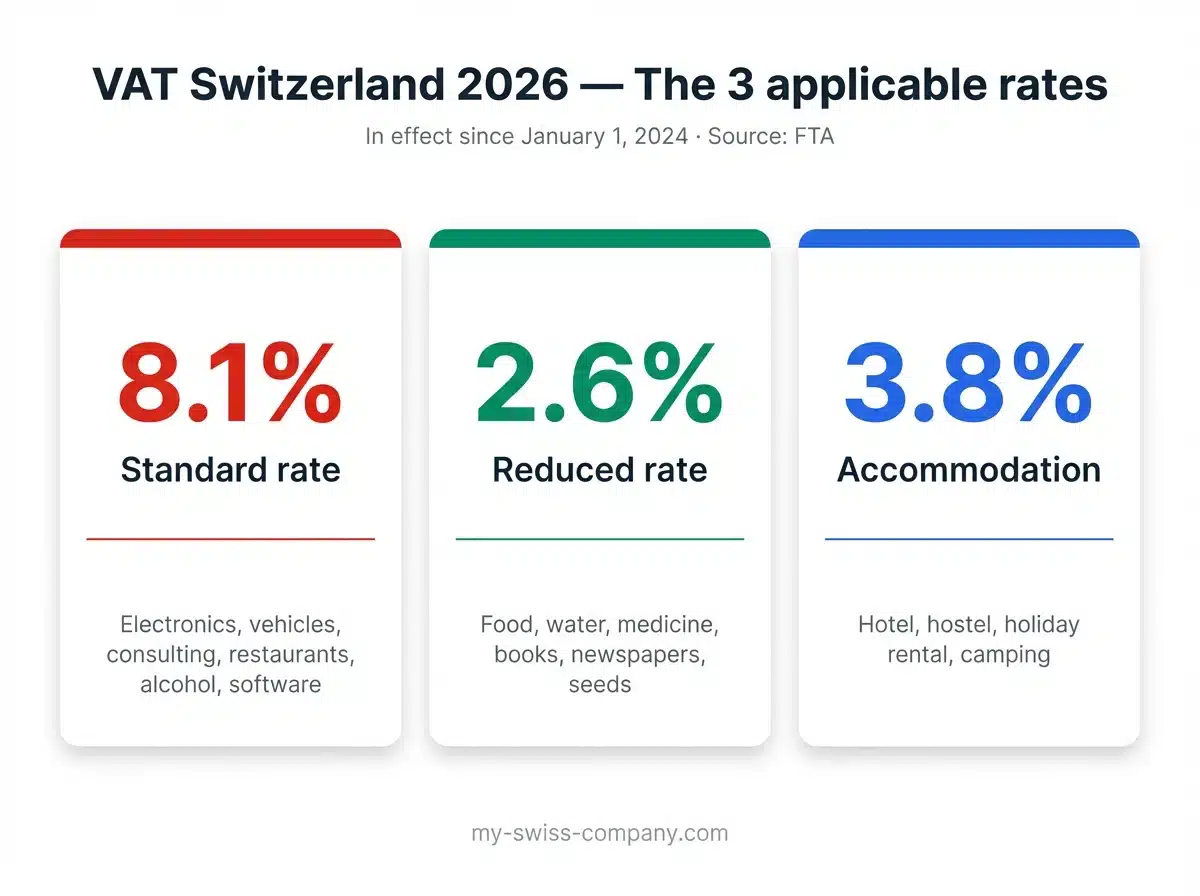

Contact our VAT expertsThe 3 Swiss VAT rates in 2026

Swiss VAT rates have not changed since 1 January 2024. They were increased on that date as part of OASI funding, following the popular vote of 25 September 2022. In 2026, the rates remain the same:

| Rate | Percentage | Goods and services covered | Rate before 2024 |

|---|---|---|---|

| Standard | 8.1% | Most goods and services: electronics, furniture, vehicles, clothing, consulting, construction, restaurants, alcohol, software, telecommunications | 7.7% |

| Reduced | 2.6% | Foodstuffs (excluding alcohol and restaurant services), drinking water, medicine, books, printed newspapers, seeds, fertilisers, menstrual hygiene products | 2.5% |

| Special accommodation | 3.8% | Hotel stays (breakfast included), guesthouses, furnished holiday rentals, camping | 3.7% |

Source: Federal Tax Administration (FTA) — Rates effective from 1 January 2024, unchanged in 2025 and 2026.

Important

Certain services are exempt from VAT (Art. 21 VAT Act): medical services, education, banking and insurance transactions, real estate rental, passenger transport and cultural events. Exports of goods outside Switzerland are subject to the zero rate (no VAT is charged, but input tax remains recoverable).

Calculation formulas: net to gross and gross to net

Swiss VAT calculation works in two directions, depending on whether you start from the net (excl. VAT) or gross (incl. VAT) price.

Calculating the gross price from the net amount

To obtain the gross amount, add the VAT to the net amount:

| Formula | Example (standard rate 8.1%) |

|---|---|

| VAT = Net × rate | CHF 1,000 × 0.081 = CHF 81 |

| Gross = Net × (1 + rate) | CHF 1,000 × 1.081 = CHF 1,081 |

Calculating the net price from the gross amount

To find the net amount from a gross price:

| Formula | Example (standard rate 8.1%) |

|---|---|

| Net = Gross ÷ (1 + rate) | CHF 1,081 ÷ 1.081 = CHF 1,000 |

| VAT = Gross – Net | 1,081 – 1,000 = CHF 81 |

My Swiss Company tip

For businesses invoicing at multiple rates (for example, a hotelier charging accommodation at 3.8% and the minibar at 8.1%), each line item must show the applicable rate and corresponding VAT amount. A Swiss-compliant invoicing software automates this process. See our article on free invoicing software in Switzerland.

Effective method vs net tax rate method

In Switzerland, VAT-registered businesses can choose between two methods for filing their returns with the Federal Tax Administration (FTA).

The effective method (Art. 36 VAT Act)

This is the standard method used by most businesses. The principle is straightforward: the net VAT due is the difference between VAT collected on sales (output VAT) and VAT paid on business purchases (input tax).

Net VAT due = Output VAT – Recoverable input tax

The effective method is particularly suited to businesses with significant VAT-liable purchases (raw materials, equipment, subcontracting), as it allows full recovery of input tax.

The net tax rate method (NTRM)

This simplified method is available to businesses with annual turnover not exceeding CHF 5,005,000 and annual VAT liability not exceeding CHF 103,000 (Art. 37 VAT Act). Instead of calculating actual input tax, the business applies a flat rate set by the FTA according to its sector, directly on its gross turnover.

VAT due = Gross turnover × applicable NTRM rate

| Criterion | Effective method | NTRM method |

|---|---|---|

| Input tax | Recovered at actual amounts | Included in the flat rate |

| Accounting complexity | Higher | Simplified |

| Turnover threshold | None | ≤ CHF 5,005,000 |

| Filing frequency | Quarterly (or monthly) | Biannually |

| Ideal for | Manufacturing, import/export, high purchases | Services, small SMEs, freelancers |

My Swiss Company tip

The choice between the effective and NTRM methods has a direct impact on your cash flow. A service company with few VAT-liable purchases (e.g. a consulting firm) will often benefit from the NTRM. Conversely, an import/export company with significant purchases will recover more through the effective method. My Swiss Company SA can run a comparative simulation to identify the most advantageous method for your situation. Contact us.

Who must register for VAT in Switzerland?

VAT registration in Switzerland is mandatory once worldwide turnover from taxable supplies reaches CHF 100,000 per year (Art. 10 VAT Act). This threshold includes turnover generated both in Switzerland and abroad — a crucial point for international businesses.

Companies registered in the Swiss Commercial Register exceeding this threshold must register with the FTA. Voluntary registration is also possible below the threshold, allowing input tax recovery. Since 1 January 2018, foreign companies providing services in Switzerland must also register and appoint a VAT fiscal representative domiciled in Switzerland (Art. 67 VAT Act).

My Swiss Company tip

For a complete overview of Swiss VAT regulations, rates and exemptions, refer to our guide on VAT in Switzerland in 2024 and 2025.

Important

Since 2019, mail-order platforms shipping goods to Switzerland must declare and pay VAT on all deliveries, with no minimum turnover threshold. The 2025 VAT reform reinforced this obligation. The FTA may prohibit the import of goods in cases of non-compliance.

VAT filing: schedule and obligations

The VAT return is the periodic declaration that each registered business submits to the FTA. The frequency depends on the method chosen and the company’s profile:

| Method | Frequency | Filing deadline |

|---|---|---|

| Effective | Quarterly | 60 days after the end of the quarter |

| Effective (large taxpayers) | Monthly | 60 days after the end of the month |

| NTRM | Biannually | 60 days after the end of the half-year |

| SMEs (from 2025) | Annually | Within 60 days of the year-end |

Since the reform that came into effect in 2025, SMEs meeting certain conditions can opt for annual filing, significantly reducing the administrative burden.

Filing is done online through the FTA online portal. Late filing incurs default interest at 4.5%.

Planned VAT increase: funding the 13th OASI pension

The Swiss VAT landscape may change in the near future. On 3 March 2024, Swiss voters approved the initiative for a 13th OASI pension, to be paid for the first time in December 2026. The funding of this additional pension is currently being debated in the Federal Parliament.

Several scenarios are under discussion:

| Scenario | Standard rate | Reduced rate | Accommodation rate |

|---|---|---|---|

| Current rates (2024–2026) | 8.1% | 2.6% | 3.8% |

| Federal Council proposal (+0.7 pp) | 8.8% | 2.8% | 4.2% |

| Council of States committee proposal (+0.4 pp VAT + payroll contributions) | 8.5% | 2.7% | 4.0% |

Source: Parliamentary debates, February 2026. A popular vote is required as the VAT change requires a constitutional amendment.

Important

No increase has come into effect as of April 2026. The current rates (8.1 / 2.6 / 3.8%) remain applicable. However, businesses would be wise to anticipate the impact of an increase on their invoicing and ERP systems. Use the projected rate simulator built into our calculator to measure the impact on your prices.

FAQ: Swiss VAT calculation

How do you calculate VAT in Switzerland?

To calculate VAT on a net price in Switzerland, multiply the net amount by the applicable rate. At the standard rate of 8.1%, the formula is: VAT = Net × 0.081. The gross amount is obtained by multiplying the net by 1.081. For the reduced rate (2.6%), multiply by 1.026, and for accommodation (3.8%), by 1.038.

How do you calculate VAT from a gross price in Switzerland?

To find the net amount from a gross price, divide the gross amount by (1 + rate). At the standard rate: Net = Gross ÷ 1.081. The VAT is the difference between the gross and the calculated net. For example, an item at CHF 540.50 gross contains CHF 540.50 ÷ 1.081 = CHF 500 net, i.e. CHF 40.50 VAT.

What are the VAT rates in Switzerland in 2026?

In 2026, Swiss VAT rates remain unchanged from 2024 and 2025: 8.1% (standard rate applicable to most goods and services), 2.6% (reduced rate for foodstuffs, medicine, books) and 3.8% (special rate for accommodation). An increase is being discussed in Parliament to fund the 13th OASI pension.

How do you calculate VAT on imports into Switzerland?

When importing goods into Switzerland, VAT is levied at the border by the Federal Office for Customs and Border Security (FOCBS). The VAT is calculated on the customs value of the goods, which includes the purchase price, transport costs and insurance. The standard rate of 8.1% applies to most imports. Businesses registered for Swiss VAT can recover this import VAT as input tax through their periodic VAT return.

What is the difference between the effective method and the NTRM?

The effective method allows full recovery of input tax (VAT paid on purchases) and suits businesses with significant purchases. The net tax rate method (NTRM) is simplified: the business applies a flat rate to its gross turnover, without detailed input tax calculations. It is available to businesses with turnover below CHF 5,005,000.

Do foreign companies need to pay VAT in Switzerland?

Yes. Since 1 January 2018, foreign companies providing services in Switzerland with worldwide turnover of at least CHF 100,000 must register for Swiss VAT. They must also appoint a fiscal representative domiciled in Switzerland (Art. 67 VAT Act). My Swiss Company SA fulfils this role for numerous European and international companies.

Sources

Conclusion

Swiss VAT calculation relies on simple formulas, but the diversity of rates, filing methods and registration obligations can quickly complicate tax management for a business. Choosing between the effective and NTRM methods, anticipating the upcoming increase to fund the 13th OASI pension, and ensuring compliance with periodic filings require structured support. My Swiss Company SA, Corporate Services Provider in Geneva, Lucerne and Zug, supports Swiss SMEs and international businesses with their VAT management: registration, filings, fiscal representation and input tax recovery.